For non-expats, currency exchange is only a concern when they come to collect their euros or dollars ahead of their summer holiday. This is followed by the annual comparison to the same transaction the previous year, and whether they received more, or less.

However, for expats, exchange rates can cause a constant headache. This is exacerbated if assets are held in different countries or there is a need to cover bills in another currency on a regular basis.

As a former expat myself, working in Switzerland and living in France added an additional layer of complexity. Being paid in CHF, paying rent in EUR, and sending money home in GBP. I would often meet clients who would be paid in CHF, receive stock from their US employer in USD and return home to Europe where they would spend EUR.

Switzerland is quite a unique example, having its own currency and being surrounded by the Eurozone. There are also a significant number of US and British expats working in the country. This made me keenly aware of the importance of currency conversation in financial planning.

If you were a British expat who moved to the EU after the millennium, you would have enjoyed an exchange rate of 1.67 EUR: 1 GBP.

That compares with 1.16 EUR: 1 GBP today, a reduction of 30.54% over that period. It would cost you 30% more to buy the same goods or services in EUR, using GBP and that is not accounting for inflation over that period. If you had made an investment in the year 2000 towards retirement, you would be looking forward to 2/3 of the lifestyle you had planned for when you made the investment.

Guaranteed pension income in another currency than the one you will spend can represent a big risk for your retirement. At Forth Capital, we advise many clients based internationally who have significant guaranteed pension income which will be payable in GBP. Although guaranteed pension income has significant advantages over invested capital, many of those advantages are eroded by weakening exchange rates.

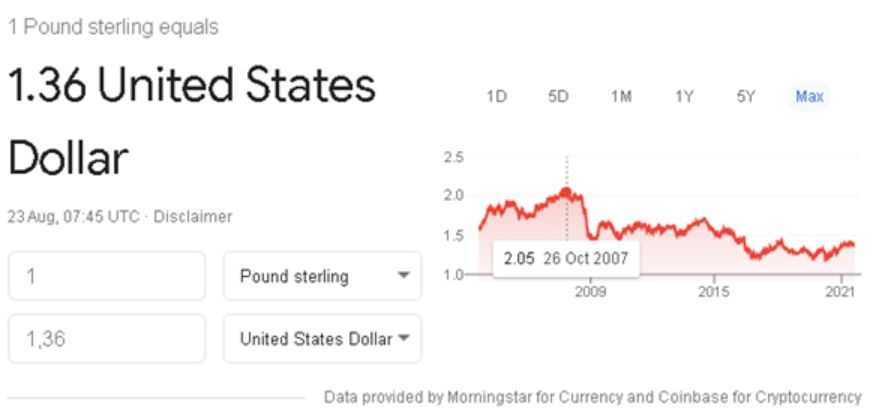

In October 2007, 1 GBP could be exchanged for 2.05 USD compared to a low of 1.22 USD in January 2017, a drop of 40% in that 10-year period.

I would imagine you would have serious conversations with your financial adviser if your investments had lost 40% over the same 10-year period.

Suddenly, a guaranteed income is not quite as guaranteed as it seemed.

At Forth Capital, we want to eliminate currency risk as much as possible. The easiest way of doing this is exchanging your funds for the currency you will spend in retirement. Then you can go back to worrying about currency when you are planning a holiday again.

However, we understand that life as an expat can change, with new opportunities arising which may mean you have to move around. There is also the pull of family and familiarity which may mean returning home eventually. The important thing is to have flexibility to save in different currencies and the expertise of a financial planner to help you to plan your journey.