Just when you thought you’d navigated the changes Brexit brought, you may now be experiencing a final sting in the tail … the loss of your UK Bank and/or Financial Adviser!

Just when you thought you’d navigated the changes Brexit brought, you may now be experiencing a final sting in the tail … the loss of your UK Bank and/or Financial Adviser!

In 2016 there were about 5,500 UK authorised financial institutions passporting their authorisations into Europe in order to look after their clients who live abroad. By 31 December 2020, they each had a decision to make – stop operating in the EU and tell clients located there that they can no longer look after them, or apply for new permissions to continue servicing those clients.

The UK was eager to limit disruption to Financial Services post Brexit, and in July 2018 introduced the Temporary Permissions Regime for EU financial firms which were using passporting to access and service clients in the UK. This provided them with a three-year grace period once the transition period ended; nothing similar was forthcoming from the EU despite a final push by the UK at the back end of 2020 to agree a way forward on this point.

Many UK financial institutions put plans in place and spent the run up to Brexit restructuring their UK businesses to account for these changes. But UK financial services firms range in size enormously and only the larger firms can more easily accommodate the new requirements. Other UK-based advice firms have only a handful of expat clients and so have decided not to apply for the new permissions.

TIME IS UP!

TIME IS UP!

In January 2021 the European Securities and Markets Authority (ESMA), felt compelled to issue a public statement reminding firms that if it is proved investment services are being provided in the EU without proper authorisation, the company is at risk of administrative or criminal proceedings, and the investors themselves may have lost the protections granted to them under the relevant EU rules, including access to any investor compensation schemes.

In addition, if your Financial Adviser is no longer authorised to provide advice in the country in which you reside, there could be an exclusion in the adviser’s professional indemnity insurance (PII). This means that should a claim arise as a result of a complaint made by you, the firms PI cover will offer no protection or redress.

While many UK financial advisers wrote to their clients in the EU requesting they appoint new advisers, others did not, and some are unaware that their clients have actually left the UK. UK firms which have retained EU-based clients, even if by accident, should also review the terms of their professional indemnity insurance (PII).

While many UK financial advisers wrote to their clients in the EU requesting they appoint new advisers, others did not, and some are unaware that their clients have actually left the UK. UK firms which have retained EU-based clients, even if by accident, should also review the terms of their professional indemnity insurance (PII).

What to look for when appointing a Financial Adviser based in the EU

Having worked in financial services for approximately 35 years (16 of those in Spain) my biggest concern for our expat community is the need to make sure that your Financial Adviser is appropriately qualified and regulated. People move to Spain and often ‘reinvent’ themselves … it could be as a joiner, builder, bar owner, estate agent, financial adviser, the list is endless! If you’ve lived in Spain for some time, I imagine you have come across a few of these ‘professionals’ … and like me may even have been caught out a few times by trusting the wrong people. Whilst there is nothing wrong with changing your occupation when moving to another country, claiming to be appropriately qualified when you are not gives professionals in any industry a bad reputation.

I’d like to explain what it means to be ‘qualified’ as for me this is by far the biggest issue. Unlike the UK, where Financial Advisers must be qualified to Level 4 to advise clients, the role of Financial Adviser does not actually exist in Spain and therefore there are no formal qualifications required in order to become a Financial Adviser. This comes as a shock to many people who meet an Adviser who is ‘suited and booted’ and automatically assume that they are both experienced and qualified in providing financial advice. Some proport to be ‘specialists’ in an area, usually pensions or investment. Check that they have the specialist qualifications to back that claim up … if they are legitimate they will be more than happy to show you their certificate!

I’d like to explain what it means to be ‘qualified’ as for me this is by far the biggest issue. Unlike the UK, where Financial Advisers must be qualified to Level 4 to advise clients, the role of Financial Adviser does not actually exist in Spain and therefore there are no formal qualifications required in order to become a Financial Adviser. This comes as a shock to many people who meet an Adviser who is ‘suited and booted’ and automatically assume that they are both experienced and qualified in providing financial advice. Some proport to be ‘specialists’ in an area, usually pensions or investment. Check that they have the specialist qualifications to back that claim up … if they are legitimate they will be more than happy to show you their certificate!

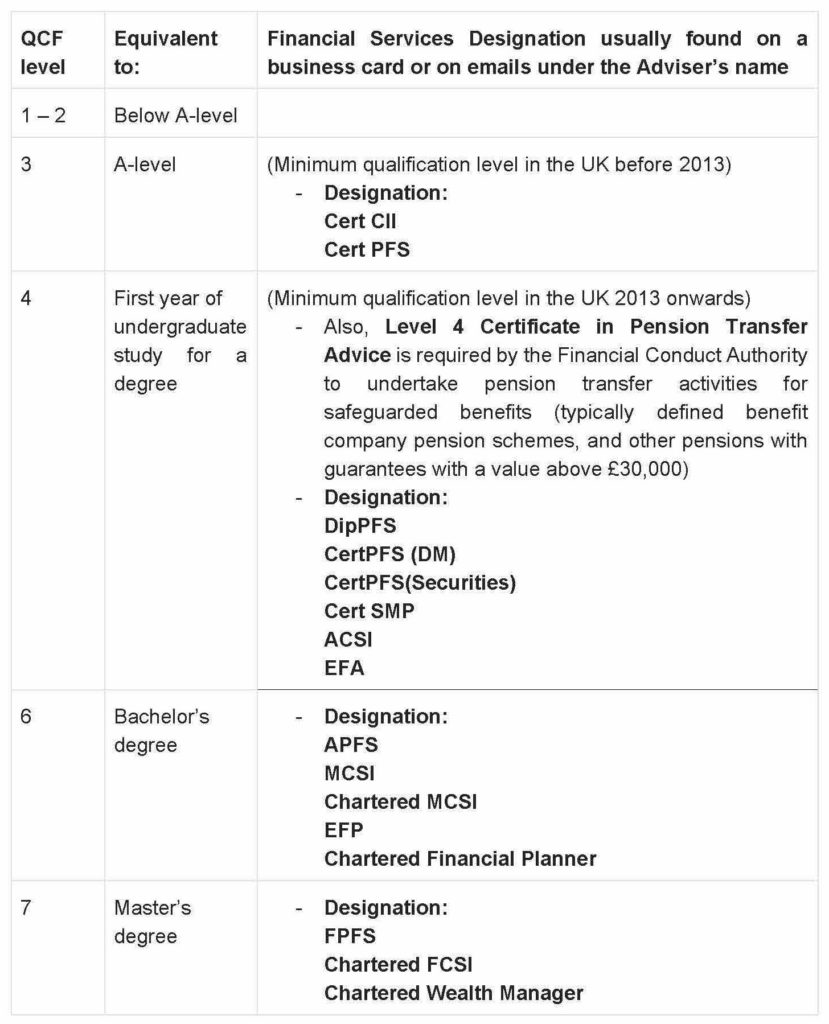

Here’s a list of the main Qualified Financial Adviser Designations to look for and where they sit in the Qualifications and Credit Framework (QCF). This list is not exhaustive, but hopefully it will give you an idea of the different levels of qualifications in the industry. To help you interpret the levels, I’ve compared them to more familiar qualifications:

This article was kindly provided by Andrea Speed from Speed Financial Solutions and originally posted at: http://www.speedfinancialsolutions.com/brexit-sting-tail-live-eu/