With 2020 behind us, we’re in a world where babies and toddlers see people wearing masks and think it’s normal! We’re also in almost negative interest rates … and that’s definitely not normal!

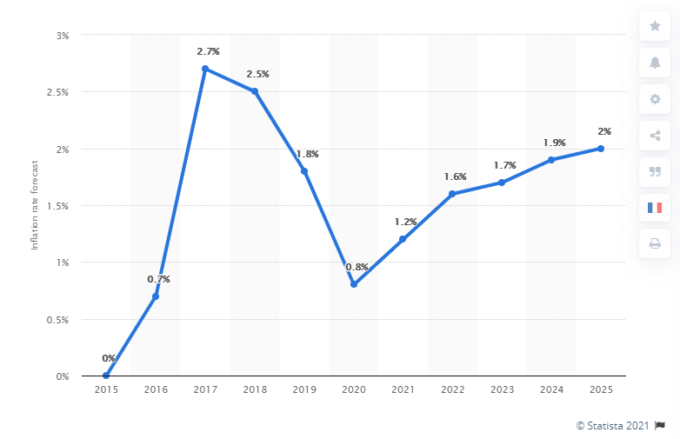

With the Bank of England’s base rate at an all-time low, savings rates have been hit hard. Whether you’ve £1 or £1 million savings in the bank you’re probably on a pitiful 0.01% interest rate. If you’re willing to tie your cash up for 3 years in a fixed rate account, you may get up to 0.9%. This still isn’t great when you consider that UK inflation is likely to hit 2% by 2025. Cash does have a function, but if you’re looking at 5 years or more you need to push further up the risk spectrum to get the returns.

Inflation

Government and Central bank policy has been to flood the market with liquidity. The downward pull on inflation that we’ve seen with the measures taken through the pandemic has put the risk of inflation increase back a little, so not something we need to think about right now, but it may well be by 2025.

UK Inflation Forecast 2025

Will we see negative interest rates?

With interest rates at rock bottom and not able to go any lower, Central banks are indicating they’re not interested in going down further into negative territory. I’d say that may come as a relief to savers but with a typical savings rate of 0.01% I’m not sure there is a silver lining to this particular cloud.

What are the alternatives?

Property – commercial property has been hit particularly hard with the onset of Covid 19. Understandable when you consider the number of people working from home and the lack of footfall on the high street. But even in good times, property tends to be illiquid.

Crypto Currency – When will crypto currency become a legitimate investment? It’s difficult to figure out where any currency is headed. Currency movement is so unpredictable but with crypto currency it’s impossible to predict. It’s been likened to a digital gold. Serious investors are trying to understand it, but we have a lot of learning to do and it’s an unregulated market which is difficult to value. Taking care (or a dare!) is key.

Bonds – Like savings interest rates, bond funds are not offering a good yield. If interest rates start to creep up, Government Bonds will fall in value. When building a diversified portfolio, we have been less keen on bonds as a balancing factor for some time.

Multi asset portfolios – The traditional split of 60% equities and 40% bonds is an old and outdated idea and much less appropriate in the current climate. If you’ve been invested solely in multi asset funds during the pandemic, you’re lucky if you’ve broken even after the market freefall back in March 2020.

Equities are the place to be. In terms of geographical breakdown, the US represents just under 50% of the total value of global markets and at the moment the US offers a ‘safe haven’ for investors. The S&P 500 is expected to hit 4,300 in 2021 and 4,600 by 2022 as we continue to see a stimulus and recovery fuelled rally. Pricey as the US stock market is, it continues to offer good growth.

Environmental, Social and Governance (ESG) – It would be remiss of me not to mention the new kid on the block … ESG funds. What does ESG actually mean for investors?

ENVIRONMENTAL – considering how a company performs as a steward of nature.

SOCIAL – examining how it manages relationships with employees, suppliers, customers, and the communities where it operates.

GOVERNANCE – looking at a company’s leadership, executive pay, audits, internal controls, and shareholder rights.

I was pleasantly surprised when I took a closer look at ESG funds. Companies that score high on the above factors tend to be better businesses in which to invest because it indicates good management, good business and good quality. So, you CAN do the right thing and it isn’t necessarily incompatible with achieving good returns. In fact, the reverse is true and you can stack the odds in your favour by including these types of funds.

The answer …

Staying alert as an investor, active portfolio management and good diversification is key, as we don’t know what’s round the corner. I didn’t see Corona virus coming … did you? We don’t know what’s going to do well and what’s not going to do well, so the way to protect yourself is to stay well diversified and ensure that changes can be made to your portfolio quickly if the need arises.The difference between mediocre return and exceptional return on your savings is made up of a number of considerations, including your attitude to risk, your time horizon, the diversification within your portfolio, the tactical equity holdings that will boost growth and the active management, including ongoing reviews of your portfolio by your Financial Adviser.

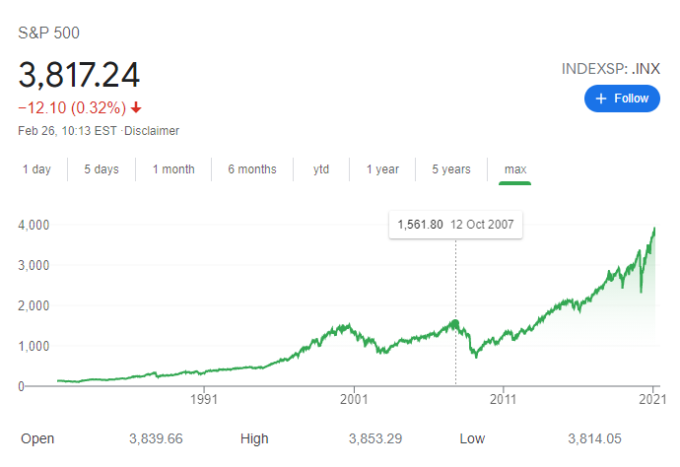

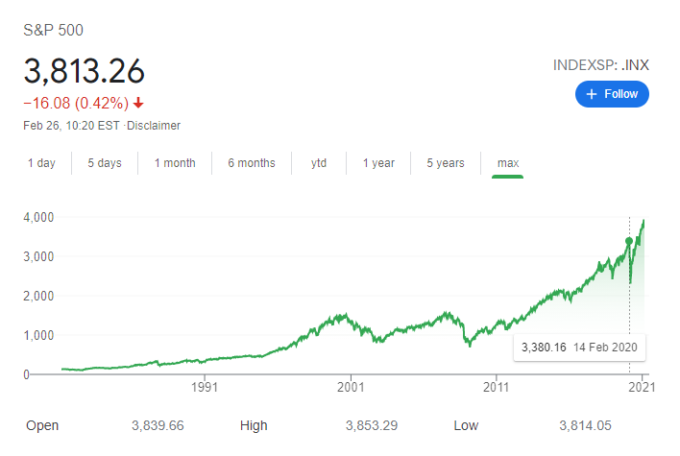

If you’re wondering whether to dip your toe in the stock market, take a look at the following charts. The first chart shows the length of the recovery following the crash in 2007/08 … it took a long time to get back to some kind of normality in the markets. The major and sudden global stock market crash we had in March 2020 after the peak in February 2020 can be seen on the second graph … the bounce back has been sharp. Now is the time to be in the markets. Shares are the new ‘safe haven’ and asset of choice in the current climate!

I recommend that you speak to us sooner rather than later as we can help you organise your savings in a way designed to minimise the tax due wherever you are resident whilst maximising growth.