The probability is that it hasn´t. However, you could have made more than 3% a year in a low risk savings plan with one of the biggest insurance companies in the world. We have many happy savers who have seen steady growth of over 3% a year for the last few years. How? Read on…

Saving money in a low interest world

Losing spending power to inflation

With special offers currently being offered by banks of 0.10% APR interest and inflation in Spain running at 1.6%, there is a guaranteed loss of the real value of money at the rate of 1.5% a year. There are some who would be disappointed, if not angry, if their money in an investment had lost 7.5% over 5 years yet this is exactly what has been happening to people over the last few years without them really appreciating it. 3% a year is not only an attractive rate of return but it is necessary to cope with inflation and provide real growth.

Spanish compliant insurance bonds

ISAs, Premium Bonds, and some other investments in the UK are tax free for UK residents. They are not tax free for Spanish residents. We are licensed to promote insurance bonds in Spain which are provided by insurance companies outside Spain but still in the EU. In fact, even after Brexit, these companies will still be EU based and so Brexit will not have the impact on these plans that it could have on UK investments. As the bonds are with EU companies, and the companies themselves disclose information to Spain on the amount invested, as well as any tax detail, the bonds are Spanish compliant which makes them extremely tax efficient. We do not deal with companies based outside the EU as we are satisfied that the regulation within the EU is for the benefit of the investor. We do not have the same confidence in some other financial jurisdictions and neither does Spain.

What investment decisions do you have to make?

Although we have the facility to personalise an investment portfolio within the parameters laid down by the EU regulators, offering discretionary fund management with some of the largest and best known investment management companies, we can also use a more simple approach for those who do not require any input into the day to day investment decisions.

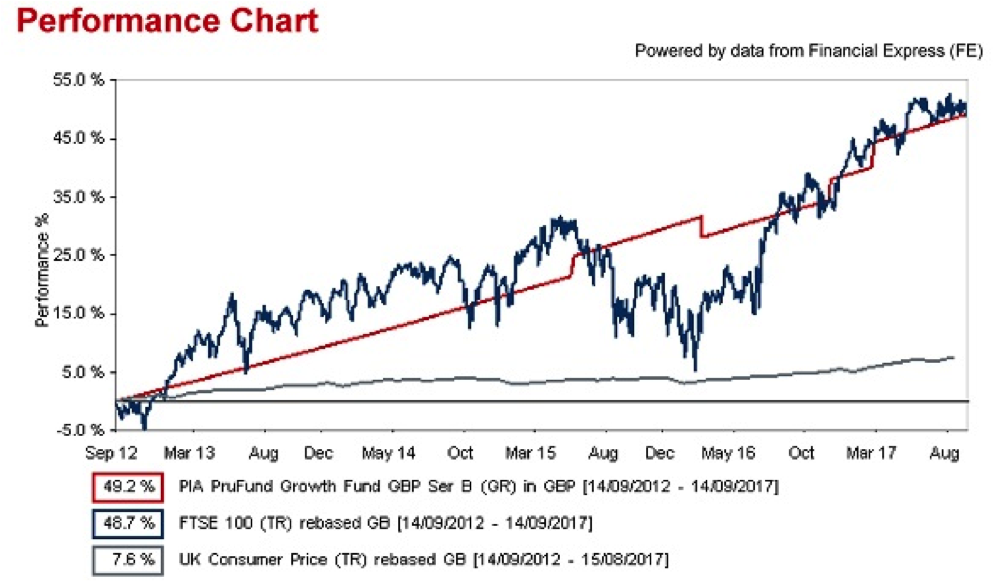

So what has happened over the last 5 years?

The chart below illustrates the performance of one of fund’s available to you compared to the FTSE100 and the UK Consumer Price index. The argument to stay invested when markets fall is valid when one looks at the FTSE100 roller coaster line with the increase we have seen over the last year or so since the Brexit vote. However, anyone accessing their money around the time of the vote could have seen a 25% drop in the investment values. Not so with the fund in the insurance bond.

Real cases

Real case 1 – £40,000 invested 24/07/12. £50,770 as at 14/09/17. Up 26.92% in 5 years

Real case 2 – £356,669 invested 10/09/14. £431,177 as at 14/09/17. Up 20.88% in 3 years

Real case 3 – £316,000 invested 05/04/16. £334,422 as at 14/09/17. Up 5.82% in 18 months

Real case 4 – £80,000 invested 13/07/16. £86,160 as at 14/09/17. Up 7.70% in 15 months

Real case 5 – £20,000 invested 27/01/17. £20,712 as at 14/09/17. Up 3.56% in 8 months

These growth rates are not guaranteed but are published to illustrate what has actually happened and that the percentage returns on the fund are irrespective of the amount invested.

How can they produce such consistency?

Each quarter, the insurance company estimates what the growth rate will be for the following 12 months. This rate is reviewed based on the views of the underlying management company with people situated in all parts of the globe specialising in their own particular area. In good times, the company will hold back money that it has made so that, when things are not so good, they are still able to pay a steady rate of growth to their savers.

I don´t want to take any risk

It is difficult to avoid risk. In fact it´s practically impossible. A risky investment is seen by many as something which has a good chance of failure, either in part or completely. Stocks and shares are seen as risky whilst putting money into a bank deposit account is not. It is generally known that stocks and shares can go down as well as up but some people are unaware, or simply ignore, the risk of keeping money in a perceived “safe” bank deposit. Bank accounts have limited protection against the bank going bust. Then, if it came to the situation where a bank had to be bailed out by the government, it could take months, if not years, to access your money. As already mentioned, if the account is making less than inflation, you are losing money in real terms. So a bank account is far from risk free. The fund illustrated above is rated by Financial Express as having a risk rating of 22% of that applicable to FTSE100, much further down the risk scale and in an area that many people feel comfortable with.

What are the charges?

We explain in detail the underlying costs. In my experience, far too many people commit to a contract without understanding what they have, having received little explanation of the terms and conditions. This is where we differ to most. Different companies have different ways of charging and we run through all of the charges so that you are happy with what you have. The real examples above have had charges deducted and so these are the real values. Your bank may not charge you for the 0.10% interest (less tax) they are paying you but they are making money through investment but not passing anything on to you even though you supplied the money they invest.

What do I need to do next?

Contact me and I can review your savings, investments, and pension funds. I can then explain how you could arrange these in a tax efficient way whilst giving you the opportunity to access the growth that is available, for an improved lifestyle and to cope with rising costs.