Savings accounts or investing in Spain – what is right for you?

This is one of the most common questions I am asked, and with interest rates creeping up I thought it prudent to run through how you should decide what’s right for you.

To help with this, firstly we need an explanation of the important differences between the two:

Why would you put money into a savings account?

Saving is putting money aside in a deposit account for the next few years. When interest rates are low, the return you’ll get on your money will be very modest. The risk is that it won’t beat inflation, which is the rate at which the prices of goods and services increase. So, whilst your money is safe (covered up to £85,000 in the UK and €100,000 in Europe), its purchasing power will be eroded over time, meaning you will be able to buy less with your money in the future. When interest rates are high you will get more return on your money, but generally in this type of economic climate it will still be less than inflation. Because of this, money you keep in cash savings accounts should be for short term savings of less than about 5 years.

Why would you invest your money?

Investing is another way of setting aside money for the future, where you invest your money into something with the aim of making a profit in the long run. When you invest, you’re generally exposed to the risk of stock market volatility (although some investments don’t invest entirely or solely in these markets). Your expected returns can fluctuate and you may not get back what you put in, especially in the short term.

You should aim for a minimum of 5 years when investing and start planning ahead with your investment strategy to manage this risk a few years before you want to access your money.

“Save for what’s around the corner and invest for the future”.

Why take any risk with your money?

Firstly, as explained above, inflation will eat into the power of your money over time. This is a problem while you are working, but is particularly important to manage when you are retired and you cannot replace lost buying power with income from your job. Secondly, not all investment risk is equal. The benefit of taking a calculated amount of risk over the long term is that it gives you the potential to make much more money than you would from a savings account, helping to pay for future large expenses and a more comfortable retirement.

What is the trend when interest rates are high compared to investing in the stock markets?

Over a short timeframe, holding cash in a savings account is usually a safe and appropriate option. It is less risky in the short term as it is readily accessible and interest rates are currently attractive relative to the past few years.

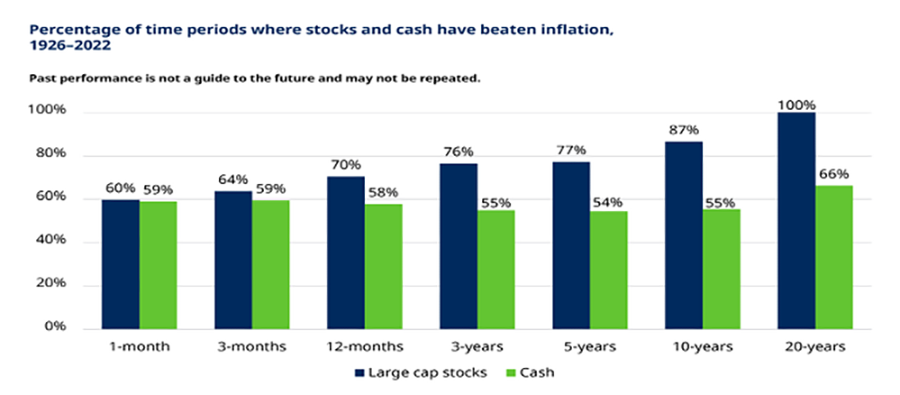

However, time is the critical factor to consider here, as over the longer term cash won’t beat inflation but investing should, as can be seen in the chart below:

Over long periods of time there is a big difference in the returns achieved from saving and investing. In the short-term, investing is riskier than an interest-bearing cash account, however when compared to inflation investing has offered far more certainty and success in the long run.

Prudential 90’s advert

Do you remember this timeless, funny classic: We want to be together!

The principles remain the same even today……

This article was kindly provided by the Chris Burke at The Spectrum IFA Group and originally posted at: hhttps://spectrum-ifa.com/investments-in-spain/

The above contents and comments are entirely the views and words of the author. FEIFA is not responsible for any action taken, or inaction, by anyone or any entity, because of reading this article. It is for guidance only and relevant professional advice should always be taken before investing in any assets or undertaking any financial planning.