In this article I will concentrate on our understanding of some of the proposed changes to the French taxation regime, as published in the Projet de Loi de Finances 2018. Of particular interest to many of our clients are the proposed changes to Wealth Tax, the increase in Social Charges and the new 30% Flat Tax on revenue from capital. At the time of writing, these, and other proposed changes have still to be agreed in Parliament and then referred to the Constitutional Council for review before entering into French law. So we won’t know for sure the exact changes that will take place until the end of the year. However, below is a brief summary of the main proposals as we understand it.

WEALTH TAX (Impôt de Solidarité sur la Fortune)

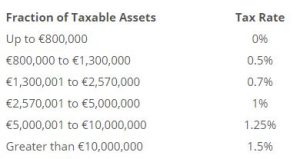

The government proposes to abolish the current wealth tax system and replace this with Impôt sur la Fortune Immobilier (IFI).

IFI would apply only to real estate assets and the principal residence would still be eligible for the 30% abatement against its value. Therefore, taxpayers with net real estate assets of at least €1.3 million would be subject to IFI on taxable assets exceeding €800,000, as follows:

This is good news for French residents with substantial financial assets, including those held within assurance vie. However, there have already been some protests to the scope of the new form of ‘Wealth Tax’ being levied only on real estate, with luxury items such as yachts and gold bullion being exempt. Thus, I don’t think we have heard the last of this!

SOCIAL CHARGES (Prélèvements Sociaux)

It is proposed to increase the Contribution Sociale Généralisée (CSG) by 1.7%. This will result in investment income and property rental income being liable to total social charges of 17.2% and, where France is responsible for the cost of the taxpayer’s healthcare in France, at a rate of 9.1% on pension income.

FLAT TAX on revenue from capital

It is planned to introduce a Prélèvement Forfaitaire Unique (PFU) at a single ‘flat tax’ rate of 30% on investment income, made up as follows:

➢ a fixed rate of income tax of 12.8%; plus

➢ social charges at the rate of 17.2% (taking into account the proposed increase).

The PFU will apply to interest, dividends and capital gains from the sale of shares.

How does this affect Assurance Vie contracts?

Based on information currently available and, of course, the finer details may change before being passed into law, it is our understanding that for premiums invested totalling €150,000 or less per person (so €300,000 for a joint life policy) the existing system of withholding tax (prélèvement forfaitaire libératoire PFL). Taking into account social charges at the increased rate of 17.2%, this results in gains on amounts withdrawn, continuing to be taxed, as follows:

➢ during the first 4 years at 52.2%

➢ between 4 years and 8 years at 32.2%

➢ post 8 years at 24.7%

The first draft of the bill proposed that the new ‘flat tax’ will replace the existing PFL system but will only apply to gains on premiums invested after 27 September 2017, that exceed the thresholds above. However, the National Assembly has already decided that it is illogical to have different tax rates, depending on how long the premium has been invested, for new investments made from 27 September 2017. Therefore, an amendment to the bill has already been proposed that all new investments made should be subject to the ‘flat tax’.

It is proposed that all taxpayers will have the possibility to opt for taxation at the progressive income tax rates of the barème scale, plus social charges. Therefore, any potential gains on capital, including withdrawals from assurance vie policies, should be assessed on an individual basis to determine in advance as to which method of taxation would be most appropriate.

There is no change to the inheritance tax treatment of assurance vie contracts and the post 8-year abatement of €4,600 for a single taxpayer, or €9,200 for a couple, will be maintained. Thus, despite the proposed tax changes, the assurance vie will continue to be a very useful vehicle for sheltering financial assets from unnecessary taxes. In addition, as assurance vie policies fall outside of your estate for inheritance tax purposes, you can leave your investments to your chosen beneficiaries without being subject to the French Succession Laws of “protected heirs”.

The abolition of taper relief

The reform also proposes the abolition of the taper relief on capital gains from the sale of shares, in respect of gains from disposals from 2018.

So, if you are sitting on a portfolio of shares which are not sheltered in a tax wrapper, then now is the time to have a look at any gains you may have and, possibly make use of the taper relief of up to 65% on the total gain, while it is still available. Don’t delay in speaking to your financial adviser who should be able to identify whether the restructuring of your investments is in your best interests.