Nerea Llona, Tax & Legal Counsel and Donna Dyason, Trust and Technical Solutions Specialist, Spain, Utmost International discuss

When your clients decide to move to Spain, it is important that they receive professional advice so that their investments continue to provide tax efficient solutions for their needs. Tax-favoured investments in the UK such as ISAs and Premium Bonds do not have the same treatment in Spain however, Spanish compliant life assurance policies provide a well-recognised and tax efficient solution for your client residing in Spain.

In this article, we highlight some key benefits of compliant unit–linked life assurance policies for your Spanish resident clients:

Legal security

Life assurance policies are highly regulated contracts, included in both Spanish and European regulations and are specifically detailed in the main tax laws in Spain, thus providing maximum legal certainty in respect of their treatment. This is as opposed to other complex structures like trusts, which are not recognised in Spain and are not efficient for Spanish tax purposes due to the fact they are looked through for tax purposes and hence do not achieve their intended purpose.

Personal Income Tax deferral

A Spanish compliant life assurance policy is a unique legal tool, which provides tax deferral benefits in Spain. This means that any growth in the policy value is not taxable until the policy is surrendered. Thus, it is not until money is withdrawn from the policy that savings income tax is due in Spain, chargeable at rates from 19% to 26%. For a policy to qualify as Spanish compliant, and hence provide tax deferral benefits, the underlying investments must meet certain requirements from policy inception, as established in Spanish Personal Income Tax Law.

Non-Spanish compliant policies do not provide this tax deferral benefit. Instead, the Spanish resident policyholder must declare the annual growth generated in their policy and pay Spanish savings income tax at the respective rate, even if there have been no withdrawals during the year.

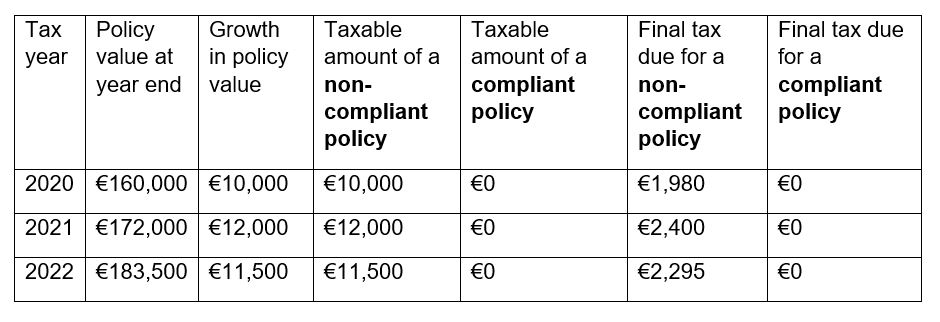

In the illustration below, €150,000 was invested in 2019 into a life assurance policy and it assumes that the policyholder has no other savings income or capital gains in the relevant tax year.

For a non-compliant policy, Spanish Personal Income Tax must be paid each year on the growth of the policy. On the contrary, with a compliant policy, if no withdrawals are taken, no Spanish Income Tax is due and the accumulated growth rolls over tax-free, maximizing the potential growth of the policy over the years:

Simplification of tax reporting liabilities in Spain

A Spanish compliant policy, where the foreign insurer reports the surrender value of the policy in the annual Form 189, reduces the reporting requirements of the Spanish resident policyholders as they would not need to include the value of their policy in the Form 720 (i.e., Informative return of overseas assets).

Additionally, when withdrawals are taken from the policy, the insurer will apply Spanish withholding tax (at 19%) and the policyholder will only pay the outstanding tax, if any, via their Spanish tax return. The insurer will provide policyholders with annual tax certificates in both English and Spanish to facilitate the completion of their tax and reporting liabilities in Spain.

Not subject to ‘Exit Tax’ and portability

These policies are not subject to Spanish ‘Exit Tax’, which is the unrealised capital gains charge for Spanish residents on their change of tax residency. For this reason, it will benefit internationally mobile families and those who will eventually relocate back to their home countries after spending several years in Spain.

Wealth solutions designed for the long term, need to be readily portable to other countries in order to meet your client’s needs and expectations, and this will be the case for life assurance policies, which will still offer tax benefits after the policyholder moves back to the UK for example.

These and other benefits, such as estate and wealth planning, can be achieved with the use of a versatile Spanish compliant life assurance policy issued by an Irish-domiciled insurer, which also has certain jurisdictional advantages. The Irish legal and regulatory framework offers one of the highest levels of asset protection available in Europe, providing an absolute preferential treatment to policyholders over other creditors as well as a robust regulatory oversight and certain tax benefits in comparison with other jurisdictions, such as Luxembourg.

To find out more about the expatriate solutions available from Utmost Wealth Solutions please contact:

James Clark – james.clark@utmostwealth.com or tel: +44 (0)7977 917396

Ryan Perkins – ryan.perkins@utmostinternational.com or tel: +44 (0)7834 499727