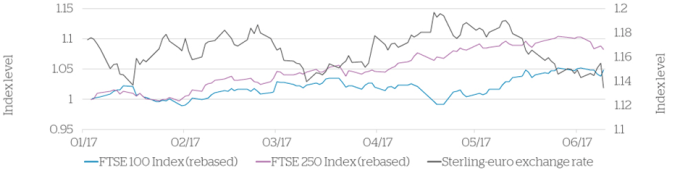

It would seem timely to offer input in respect of the effect of the UK General Election results on the markets. The hung parliament result has further complicated the political backdrop and increased uncertainty surrounding the UK’s forthcoming Brexit negotiations. A weakening of sentiment initially put UK equity markets under pressure, but sterling’s declines have since supported the FTSE 100 Index. On the other hand, the domestically-focused FTSE 250 has experienced minor declines. This situation can be explained by the FTSE 100’s large multinational constituents deriving a benefit from sterling’s depreciation, as it boosts the value of the revenues they earn overseas, while the FTSE 250 is perceived to be more exposed to domestic political risk.

The balance of factors looks less supportive for domestic UK equities, but stocks with earnings overseas should continue to benefit from the boost to earnings provided by a weaker Pound.

With 321 seats needed in practice to form a majority, a second election in the autumn looks possible, with a left-wing Labour government a conceivable outcome.

The results were as follows from 8 June 2017:

| Party | Seats |

| Conservatives | 318 |

| Labour | 261 |

| SNP | 35 |

| Liberal Democrats | 12 |

| Democratic Unionists (DUP) | 10 |

| Sinn Fein | 7 |

| Plaid Cymru | 4 |

| Green | 1 |

| UKIP | 0 |

Meanwhile, the EU may see the current situation as an opportunity to be tougher in terms of departure. However, lower support for the SNP also means that the threat of Scottish separatism appears to have diminished.

Outlook for Investors

We are extremely positive on the prospects for value equities. Trump\’s presidency means that active management, including stock picking, will come into its own. The key is to maintain liquidity to ensure tactical moves can be made. Since the Spring of 2016 US equities have performed well, whilst European equities have lagged behind somewhat. As ever with equities, the price you pay is a key determinant of the returns you can potentially make. In our view, European equities now look attractive from a valuation standpoint.

One reason why European equities have lagged other regions is that we have witnessed several years of earnings declines. Some of this has been due to pressure on the financial sector, as well as the effects of low commodity prices.

However, we think 2017 could see European corporate earnings grow at their fastest rate in five years and so for our clients it’s important that we have sufficient exposure to European equities to take advantage of this growth.

Always consider your investments as a whole and make sure your adviser is rebalancing your portfolio as appropriate in order to take advantage of the current economic climate. Low risk usually leads to lower long term returns, interest rates on savings accounts have been at an all-time low for some years and this trend is likely to continue to worsen. Of course, everyone should have some cash for emergencies and unexpected events, but for those with a longer term investment outlook (5 years or more) this should be supplemented with investments in other asset classes and geographical spread that offer better potential for real capital growth and/or income.